Into the multiplex

At the UN General Assembly in late February, on the anniversary of Russia's 2022 invasion of Ukraine, the U.S. voted against a Europe-led resolution affirming Ukraine’s territorial integrity, proposing a watered-down peace resolution without criticism of Russia. This followed JD Vance's dressing down of European leaders for their political failures at the Munich Security Conference.

Europe is now operating on the assumption that the post-war U.S. security guarantee is gone: first by increasing defense spending and coordination among EU and other NATO members.

The UN and multilateral system, also built on this U.S.-backed international order, is stuck figuring out its own political and financial reckoning.

The overhaul of U.S. foreign policy is right now centred on trade and tech: threatening tariffs and rewriting bilateral deals, seemingly to protect U.S. industries. The White House issued a memo to counter currency “misalignment” and review WTO commitments, also blocking a foreign takeover of a U.S. steel company on national security grounds, while emphasizing control of critical tech and supply chains. In its final weeks, the Biden administration set new export controls targeting Chinese tech sectors. Trump mooted expanding restrictions and leveraging U.S. market power to secure concessions.

The U.S. has prioritized infrastructure deals: agreements with allies on secure 5G networks and digital infrastructure. U.S.–Ukraine discussions on critical minerals led to a preliminary deal to ensure U.S. access to lithium and rare earths in exchange for reconstruction aid.

These first months of 2025, U.S. foreign policy has reset the international order toward unilateral, nakedly interest-driven deal making, within a unstable arrangement of overlapping spheres and sectors. Trump's rejection of multilateral agreements, including denouncing the 2030 Agenda and withdrawing from the Paris climate agreement, the future of multilateral forums and frameworks looks bleak.

International organisations' capacity and mandate to uphold norms are being openly challenged, the wider international community is facing a reckoning in this sudden crisis of the liberal international order, without a clear resonating response on how to reorganise trade, security and development financing in the face of a new, dynamic and layered 'multiplex' world order.

Pragmatic Fractured Trade

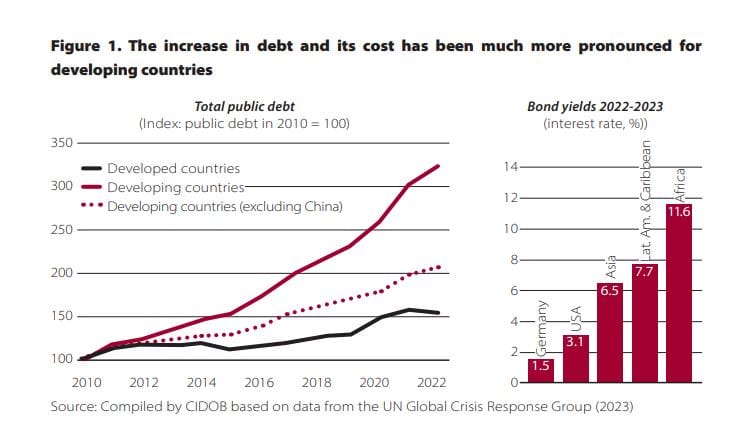

Developing countries, strained by the pandemic and slowing growth, face a debt and trade deficit crises. The G20’s Common Framework for Debt Treatments, launched in 2020 to coordinate creditors (including China) for low-income country debt relief, has had limited success – delivering relief only after protracted delays in cases like Zambia and Ghana. Under South Africa's presidency, the G20 is reviewing the Common Framework at its five-year mark to address complaints that relief has been “too little, too late, and too complex”.

As the largest official creditor to many African and Asian nations, China’s cooperation is needed for any effective debt workout. The inclusion of Chinese state banks in joint creditor committees (alongside Paris Club members) in Zambia’s and Ghana’s deals was promising, but negotiations were slow to expedite future cases, proposals include automatic standstills on debt service during negotiations and use of state-contingent debt instruments (linking repayments to growth or commodity prices) to share risk (odi.org). Another idea gaining traction is expanding the IMF’s use of issuing Special Drawing Rights (SDRs) automatically during global shocks and allocating them by need, not quota, to provide emergency liquidity to vulnerable states. These might start to reshape the international financial architecture to be more responsive to the needs of the Global South (cidob.org).

As multilateral trade liberalization stagnates, countries are reorganizing commerce around strategic blocs and bilateral deals. The United States and EU have increasingly “friend-shored” and diversified away from adversaries: in 2024, U.S. imports from China declined while imports from Mexico, Vietnam and other partners rose – sometimes by routing Chinese components through those countries. Europe, in turn, drastically cut trade with Russia after 2022 (due to sanctions) and deepened trade with the U.S. and alternative energy suppliers. China has reoriented its trade toward emerging markets: as of 2024, developing countries account for the majority of China’s trade, reducing reliance on U.S. and EU markets (mckinsey.com). New alliances and regional agreements among the Global South are expanding South–South trade at a rapid clip. For instance, the African Continental Free Trade Area (AfCFTA) and an expanded BRICS+ grouping are facilitating more trade, sidestepping Western blocs.

In late 2024, the EU and Mercosur (South America) reached a free trade agreement after 20 years of talks which, while still shaky, signals a bridging of Northern and Southern economies. Major economies like India are emerging as swing players – India’s trade is growing with both Western and Eastern blocs. India has leveraged its non-aligned stance to sign trade pacts with partners ranging from the UAE to Australia, while also benefiting from “China+1” supply chain strategies that see manufacturers invest in India as an alternative to China (bcg.com).

These realignments reflect the potential in a more pragmatic version of a multipolar and fragmented trade system. Regional and issue-specific trade agreements are filling gaps left by WTO withdrawels – from the RCEP in Asia (anchored by China and ASEAN) to the CPTPP (driven by mid-sized Pacific economies). In this more complex global trading architecture where influence is again more openly contested, the global-level multilateral institutions are yet to fully adapt to these shifts in power and norms, as countries form parallel coalitions (e.g. the G7’s “economic resilience” working group, or BRICS trade cooperation) that could either complement or undermine the universal trading system.

A thicket of security arrangements

The U.S. shift from NATO to smaller, regional security arrangements like the Quad (U.S., India, Japan, Australia) and AUKUS pact (Australia, UK, U.S.) could prove more flexible for deterring China. Meanwhile, China and Russia have strengthened their strategic ties, conducting joint military exercises and promoting blocs like the Shanghai Cooperation Organisation (SCO). Middle powers are asserting more autonomy in multi-vector diplomacy – Turkey balancing NATO membership with SCO outreach, Saudi Arabia joining China-led security dialogues while maintaining U.S. links. In the Middle East, regional-led diplomacy has grown (e.g. the China-brokered Saudi–Iran normalization in 2023, and the Abraham Accords (between Israel and Arab states). In Africa and Latin America, regional organizations (African Union, CELAC, etc.) and ad hoc coalitions are addressing conflicts with less external interference.

Major economies are more explicitly and deliberately linking economic and security initiatives. The U.S.-EU coordination on technology (through the TTC) also serves security aims – ensuring allied access to semiconductors and blocking exports to rivals. China’s Belt and Road Initiative now more openly pursues military basing and arms sales in partner countries. Economic security has taken center stage: countries impose export controls on strategic goods (like advanced chips, or as China did in 2023 on gallium and germanium for semiconductors) under national security justifications.

If the line between global economic governance and security competition disappears, multilateral institutions are going to have to directly address the security externalities of trade, investment and sustainable development pathways, including the complex energy security and disaster risk management at the centre of climate finance negotiations.

Financing competitive international cooperation

With Trump adding explicit conditionality to the US underwriting of European security, namely in Ukraine, European and other NATO allies are increasingly isolated in their contest with Russia. The Global South are largely ambivalent about Western rivalry with Russia and China, yet have suffered from the initial disruptions of the Ukraine war to grain exports, energy prices and supply chains, and then to the diversion of ODA from traditional aid donors towards Ukraine aid and towards domestic European refugee resettlement.

The UN’s Summit of the Future, at the GA opening last September, tabled ambitious ideas to update global governance – like doubling development finance from multilateral development banks to $500 billion/year and simplifying global tax rules. The modest UN environmental 'COP' conference outcomes in late 2024, and outlook for a new Financing for Development agreement in July will need to seek a way to reform or accommodate the BRICS’ New Development Bank, Asian Infrastructure Investment Bank and regional trade blocs taking on larger roles. On top of this, a new sustainable development framework will likely begin to be negotiated to succeed the 2030 Agenda.

Early 2025 has put to rest any doubt that the UN and multilateral organisations need a more fundamental version of 'reform' to survive. Just as the 'realpolitik' Security Council underpinned the UN's normative, peace and development achievements in the 20th Century, the UN now needs a new way to channel increasingly complex, fragmented and competitive modes of cooperation that underpin this new global order.

A new infrastructure of financial, data and technology platforms will be needed to support this new multilateralism - the 'physical and organizational capability of a system to move ideas, goods, people, and money' - that meets countries and their people where they actually are: a messy, disturbing world.